The Necessity of Carbon Markets

How market mechanisms can turn economic forces that once drove emissions into powerful tools for environmental good.

A history of unpriced externalities

Climate change threatens to have a catastrophic impact on the planet's ecosystem within our lifetimes. To avoid climate breakdown, we must slash carbon emissions to net-zero by 2050. This piece examines why carbon markets are essential to achieving our climate goals. Looking at the economic forces behind historic emissions illuminates why carbon markets are a critical tool for incentivizing decarbonization, carbon capture, and ecosystem restoration.

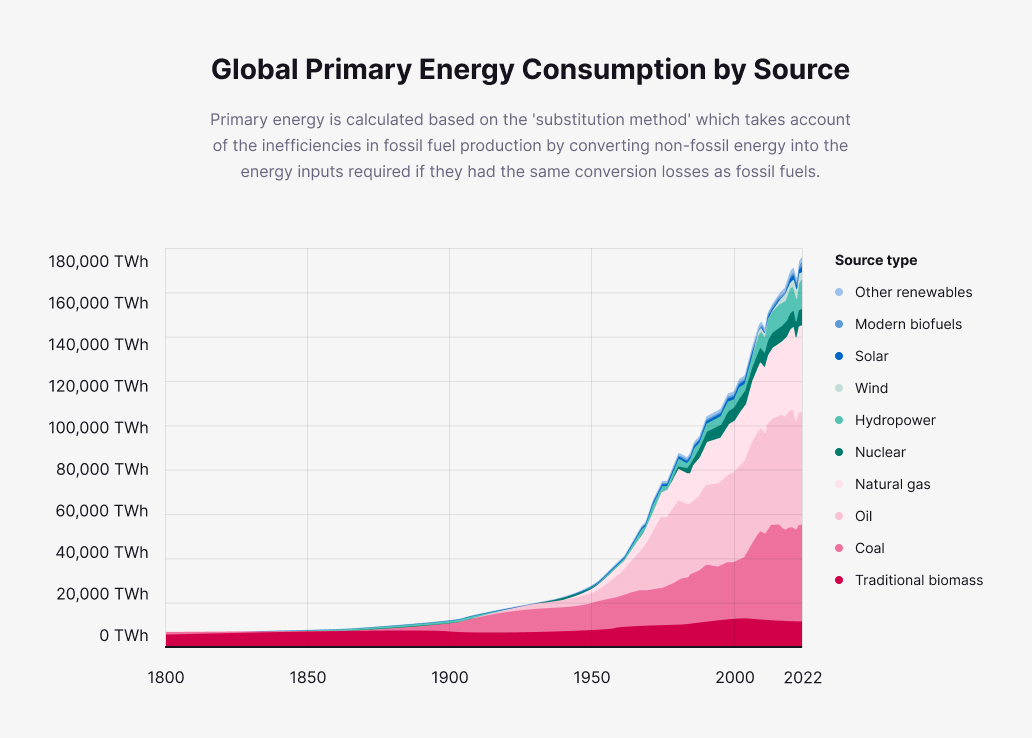

In the 200 years since the onset of the Industrial Revolution, most of the world has coordinated economic production through some form of free market capitalism. Countries have predominantly adopted mixed economies that combine free market elements with some degree of state intervention. A key feature of capitalist systems is the pursuit of economic growth, defined as the increase in production and consumption of goods and services measured via gross domestic product (GDP). Growth has historically been achieved through the manufacturing of goods, from industrial machinery to consumer products. In essence, capitalist economies are structured to incentivize the continuous expansion of production and consumption to create robust GDP growth figures and sustain financial markets.

In pure market capitalism, negative externalities are not priced into production and consumption costs. These are the side effects that occur when producing or consuming a good imposes costs on third parties not involved in the transaction. They represent a common but decisive market failure, as broader social costs are not reflected in the price that producers or consumers pay. In other words, market pricing only captures private costs rather than total societal costs. This divergence leads to overproduction and overconsumption compared to what would be optimal for a society. Environmental pollution exemplifies this: factories can release pollutants without bearing cleanup costs and our biosphere, and the people and animals that live under it pay the price. Regarding carbon dioxide emissions, it is the earth’s atmosphere that has been treated as a free waste repository.

This unchecked rise in emissions over the past two centuries exemplifies the "tragedy of the commons" articulated by ecologist Garrett Hardin. He described how individuals acting rationally in self-interest will collectively overexploit and destroy a shared resource. Concerning climate change, the atmospheric capacity to absorb some greenhouse gas emissions (GHGs) without any warming has resulted in the earth’s atmosphere becoming an unpriced global "commons", which human economic activity has abused. Each country and firm individually benefits from unrestrained emissions fueling growth, while the costs have been diffused across the world's population. This, and the absence of constraints led to a relentless climb in industrial CO2 emissions over the past two centuries as industries have used the cheapest input sources, irrespective of their GHG implications. The energy sector exemplifies this dilemma: it still produces 80% of energy from fossil fuel, GHG-emitting sources.

With no price tag applied to emissions, there have been no market forces with sufficient power to constrain the resulting accumulation of GHGs. Atmospheric carbon dioxide levels therefore markedly increased following the Industrial Revolution, rising from under 300 parts per million (ppm) at the start of the twentieth century to over 400 ppm today.

Historically, the implications of rising atmospheric carbon dioxide and climate change have not gone unnoticed. As early as the 1930s, Guy Stewart Callendar argued that the earth was warming due to accumulating industrial emissions. The theoretical groundwork was laid even earlier, as far back as the 19th century, by scientists like Joseph Fourier, who described the greenhouse effect. Later, increasingly sophisticated computer models allowed more precise climate projections. To further compile climate science for policymakers, international bodies like the Intergovernmental Panel on Climate Change (IPCC) were established to provide regular assessments synthesizing the research of thousands of scientists worldwide. Multiple lines of evidence have thus mounted since the 19th century that clearly and convincingly demonstrate the climate impacts of rising carbon dioxide levels.

In 1992, the accumulated scientific evidence eventually compelled the UN to hold the Rio Earth Summit, which adopted the United Nations Framework Convention on Climate Change (UNFCCC). The UNFCCC's objective was "to stabilize greenhouse gas concentrations in the atmosphere at a level that would prevent dangerous anthropogenic interference with the climate system". The UNFCCC represented a turning point where the definitive scientific consensus on climate change risks finally mandated policy action on emissions. This goal of stabilizing GHGs was made more tangible in the 2015 Paris Agreement, which draws on data from the IPCC and ratifies a commitment to prevent global temperature rise exceeding 1.5°C above pre-industrial levels to prevent the worst effects of climate change.

A market-based solution

What is not explicitly stated—and in fact is taken as a given—in both the UNFCCC and the Paris Agreement is that achieving climate stabilization must occur within the framework of today's capitalist economic system. As a result, finding a way to reconcile the drive for economic growth within quasi-free markets with the necessity of reducing GHGs to combat climate change is the critical challenge of the 21st century. To meet established emissions reduction goals and temperature targets, net-zero human-caused CO2 emissions must be accomplished by 2050.

There are currently two core market failures relating to climate change: 1) That emitting CO2 is free of charge, an unpriced negative externality, and 2) that sequestering CO2 is unpaid, an unpriced positive externality. The way governments often intervene to correct for market externalities is via taxes that disincentivize negative externalities and subsidies that promote positive externalities. In the case of carbon, directional incentives are insufficient as we need to precisely limit carbon emissions to meet our specific climate goals. Subsidies for activities that are difficult to measure, such as reforestation activities, are also challenging for a government to implement correctly. Carbon markets are an elegant solution to address both these issues with a two-pronged approach:

- Compliance markets, such as the European Union Emissions Trading Scheme, set limits on a country or region’s emissions and allows companies to trade the rights to emissions under that cap. Critically, these programs provide specificity around decarbonization paths as the total emissions are capped and can be reduced year over year. They also allow for market pricing to occur.

- Voluntary carbon markets put a price on the positive externality of sequestering carbon, converting it from something that only benefits the commons, to a “private good”. It does so by issuing carbon credits that are paid for by buyers who claim the benefit of the positive externality. This provides a mechanism to fund the removal of carbon from the atmosphere.

In the future, these two markets may merge, with the price of carbon emissions going directly towards the sequestration of CO2. See our Convergence of Voluntary and Compliance Carbon Markets article for a deeper dive into this topic.

These markets are not just an elegant solution for guiding decarbonization and funding sustainable activity, they are essential for achieving our net-zero goals. Estimates vary, but optimistic projections indicate that hard-to-abate emissions or emissions that will be too difficult or expensive to eliminate will be 3 billion (CDR experts) to 10 billion (National Academy of Sciences) tons per annum – requiring equivalent carbon removals to achieve net-zero. Even after reaching net zero, ambitious climate goals necessitate "net negative" global emissions in the latter half of this century to compensate for historical emissions and bring us back to pre-industrial temperatures.

All of the above assumes that we achieve our decarbonization and 1.5C goals. However, recent reports indicate that we are increasingly unlikely to do so. Major course correction is needed in order to maintain temperatures below 1.5C (BCG report). Current data shows emissions growing 1.5% year-over-year between 2011 to 2021 with 7% annual reductions now needed through 2030 to meet 1.5C, a seemingly unlikely reversal. Deviations from achieving our goals will require significant removals to compensate, according to CarbonBrief:

“Specifically, each 0.1C of temperature overshoot above 1.5C will require the deployment of around 220 GtCO2 (~5.5 years of current global emissions) additional CDR to bring temperatures back down after net-zero CO2 emissions are reached.”

While decarbonization and sequestration pose the larges challenge, we also need to support and finance ecosystem preservation and restoration. Forest loss continues to outpace reforestation globally, leading to the degradation of crucial carbon sinks and biodiversity collapse. The State of Climate Action Report 2022 illustrates these trends and shows that we need to reforest 100 Mha and reduce the annual rate of deforestation to 1.9Mha a year from the current 5.7 Mha to meet our 1.5C target:

The VCM can address this concerning trend by channeling finance into verified reforestation and avoided deforestation projects. Such nature-based solutions can preserve existing carbon stocks and regenerate new forests to sequester additional CO2.

A long road ahead

Carbon markets are expanding. Nevertheless, we still have a lot of work to do. According to the World Bank’s Carbon Pricing Dashboard, only 23% of GHGs are regulated by compliance carbon markets, including both cap and trade and carbon tax schema. The remaining emissions currently need to be addressed via voluntary action. Among the largest 2,000 public companies, however, only around half have some type of net-zero target:

That said, companies that do purchase carbon offsets are also working hard on decarbonization. In research from 2023, Sylvera found that utilization of carbon credits actually correlates with more aggressive internal emissions reductions:

"On average, companies that buy carbon credits are simultaneously cutting their Scope 1 and 2 emissions by 6.2% per year. Meanwhile, companies that don’t use carbon credits are cutting emissions by only 3.4% per year."

In other words, companies that are making credit purchases in the VCM are also cutting their direct emissions at almost twice the rate of companies with no carbon market exposure. They are leading the way to net zero.

Of course, even as more and more companies implement forward-thinking net-zero plans, some emissions will remain unavoidable even after maximizing reductions. The reality is that the full decarbonization of operations and value chains is an enormous challenge.

Similarly, transitioning the global economy to run on clean energy will also take time. High-quality carbon credits provide a path for companies to neutralize these irreducible emissions in the interim—enabling carbon neutrality while pursuing an ambitious transition strategy. Prominent organizations explicitly recognize certified offsets as an essential tool for bridging unavoidable GHGs, and major corporations have incorporated them into their science-based net-zero plans. For example, the energy firm Ørsted, whose GHG commitments have been validated by the Science Based Targets Initiative, is aiming to achieve net-zero emissions across its value chain by 2040, including offsetting the final 1% of stubborn emissions via certified removal projects like mangrove reforestation.

Assessments of how much the carbon market needs to grow vary markedly, but insights from organizations such as Morgan Stanley, Bloomberg, and McKinsey all predict exponential growth through 2030 and beyond. Predictions have been made of a hundredfold increase, while others suggest the global carbon market will be worth upwards of a trillion dollars by mid-century. While debates on its required scale vary, its necessity is clear: carbon markets are crucial for achieving net-zero.

Neutral is an exchange for environmental assets. We combine tokenized carbon credits, renewable energy credits, and carbon forwards with specialized market infrastructure to deliver efficiency, transparency, and trust in these markets.